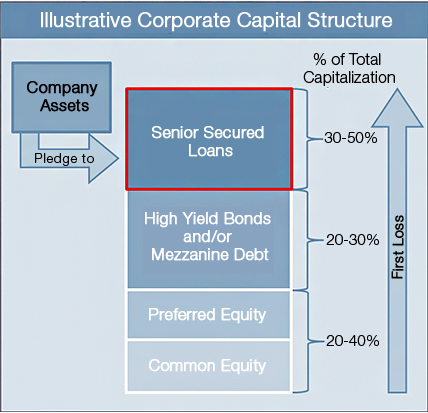

The corporate capital structure highlighted above is a hypothetical structure and for illustrative purposes only. Corporate capital structures may vary substantially from the hypothetical example set forth above.

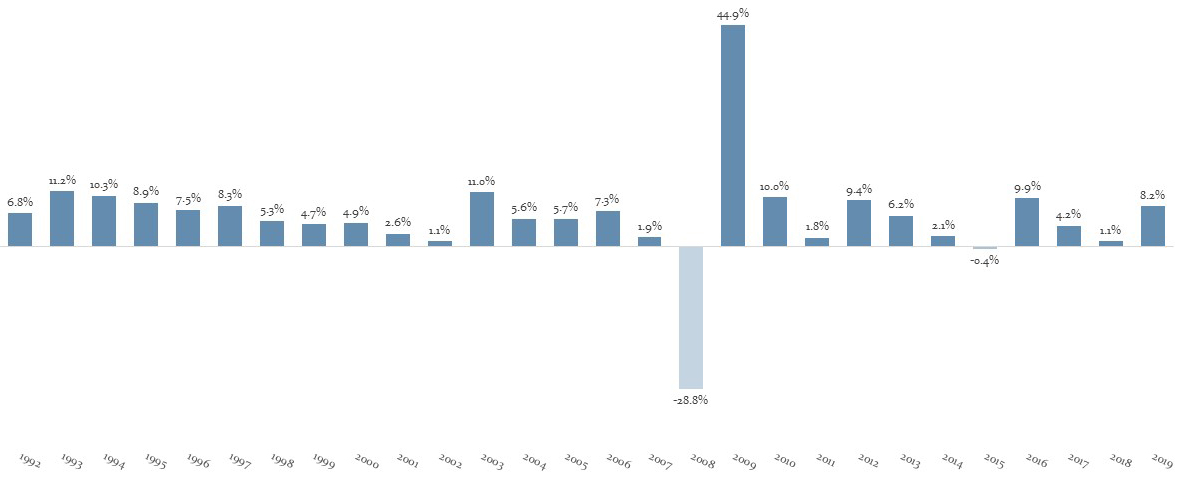

Source: Credit Suisse. Past performance is not indicative of, or a guarantee of, future performance. The Credit Suisse Leverage Loan Index tracks the investable universe of the US-denominated leverage loan market. Index returns do not reflect any deductions for fees, expenses or taxes. You cannot invest directly in an index.

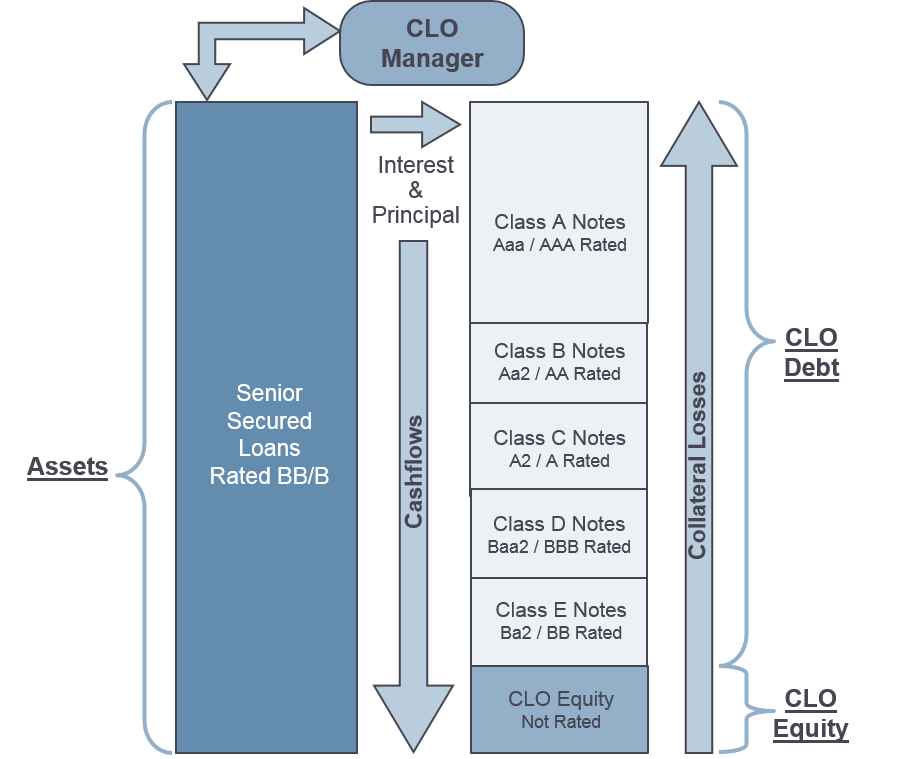

The CLO structure highlighted above is a hypothetical structure and for illustrative purposes only. CLO vehicles may vary substantially from the hypothetical example set forth above.